Surgery Center Valuation: Complete Guide to ASC Valuation Multiples and Methods

Understanding surgery center valuation is essential for investors, healthcare professionals, and ASC owners navigating the complex landscape of ambulatory surgery center transactions. Whether you’re considering buying, selling, or partnering with an ASC, knowing how to accurately determine value using industry-standard multiples can mean the difference between a profitable transaction and leaving money on the table.

This comprehensive guide explores the intricacies of surgery center valuation, from EBITDA multiples to key factors that influence ASC worth in today’s healthcare market.

Nechay Appraisals provides ASC valuations for physician-owners, investors, and healthcare professionals nationwide. Whether you need a valuation for a physician buy-in, partner buyout, or full sale, we deliver credible, defensible appraisals backed by deep ambulatory surgery center experience. Schedule a free consultation to discuss your ASC valuation needs.

Key Takeaways:

- Surgery center valuation multiples typically range from 2x to 8x EBITDA, depending on size, specialty mix, payer composition, and whether you’re valuing a controlling or minority interest

- EBITDA multiples are the most common transaction metric, though formal fair market value appraisals using multiple methodologies are equally prevalent in practice

- Size, location, payer mix, specialty focus, and operational efficiency significantly impact valuation multiples

- Multi-specialty centers generally command higher multiples than single-specialty facilities (7x–8x vs. 4x–6x for controlling interests)

- Controlling interests trade at substantial premiums over minority positions

- Heavy out-of-network revenue concentration can eliminate most buyers or warrant significant multiple reductions

- In CON states, existing ASCs often command premium valuations due to barriers to entry

Table of Contents

What Are Surgery Center Valuation Multiples?

Surgery center valuation multiples are financial ratios used to determine the market value of ambulatory surgery centers by comparing their financial performance to established benchmarks. These multiples provide a standardized method for evaluating ASCs against comparable facilities and transaction data.

One of the most common approaches to surgery center valuation involves applying a multiple to the center’s Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA). This methodology allows buyers, sellers, and investors to quickly assess value based on the center’s earning potential.

Understanding surgery center valuation multiples requires examining several key components:

Market Value of Invested Capital (MVIC): This represents the total value of a surgery center, including both equity and interest-bearing debt. The formula for calculating valuation using multiples is:

MVIC = EBITDA × Valuation Multiple

In practice, you’ll also see valuations expressed in terms of Enterprise Value (EV). The key difference: MVIC treats cash as an operating asset included in the value, while Enterprise Value excludes cash (and is calculated as equity value plus debt minus cash). Understanding which metric is being used prevents confusion when comparing deal terms or valuation reports.

Financial Metrics: While EBITDA is most common, valuation multiples can also be based on revenue, net income, or cash flow. Each metric serves different purposes depending on the ownership structure and transaction type.

Formula Method vs. Fair Market Value Appraisals

In practice, ASC ownership transactions use one of two approaches to determine value:

Formula Method: Many ASC operating agreements specify a predetermined formula for buy-ins and buyouts. Shareholders agree in advance on a financial metric (e.g. EBITDA) and a fixed multiple (e.g., 4x or 5x). When a transaction occurs, the parties simply apply the formula to current financials. This approach offers simplicity and predictability — everyone knows the rules upfront, and there’s no negotiation over methodology.

However, formula methods have drawbacks. A fixed multiple doesn’t account for changes in market conditions, shifts in case volume, payer contracts, or operational improvements. A center that’s growing rapidly or one facing a drop in utilization will be misvalued using a formula approach. The formula method is a pricing mechanism, it doesn’t consider the actual return (think dividends) that the investor will receive from ASC ownership.

Fair Market Value Appraisal: Other ASCs require an independent appraisal for each transaction. A certified appraiser analyzes the center’s financials, market position, and comparable transactions to determine value at the time of the buy-in or buyout. This approach captures current market conditions and center-specific factors that a fixed formula might miss.

Both approaches are common. Formula methods reduce transaction friction but can produce values that diverge from actual market conditions over time. Appraisals add cost and complexity but provide a more accurate picture of what the interest is actually worth.

Current Surgery Center Valuation Multiples: Market Data and Ranges

ASC valuation multiples vary based on two primary factors: specialty composition and control level.

Disclaimer: The valuation multiples presented here are for educational purposes only and do not constitute valuation advice or represent the professional opinion of Nechay Appraisals or its analysts. For advice specific to your practice, consult a qualified valuation professional.

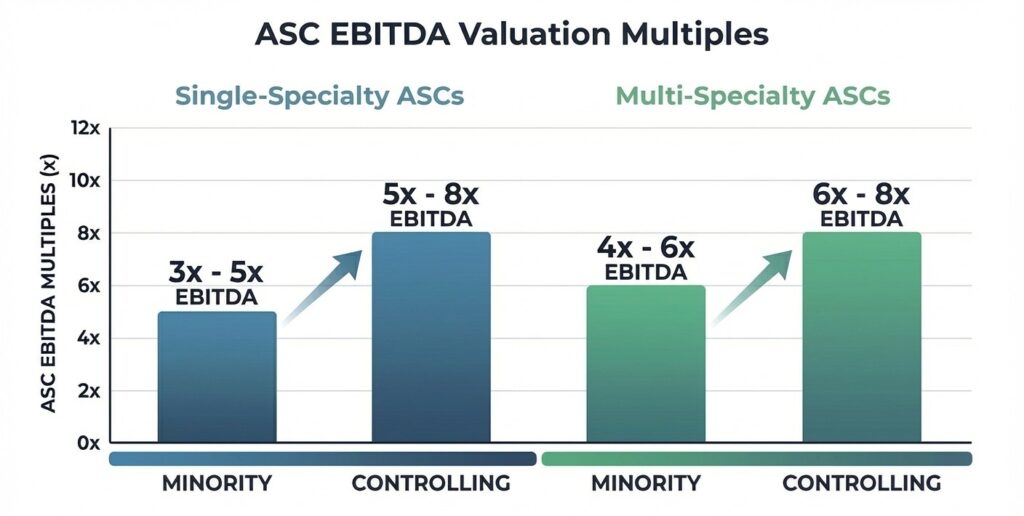

Single-specialty ASCs typically trade at lower multiples than multi-specialty facilities. For minority interests in single-specialty centers, multiples commonly fall in the 3x–5x EBITDA range, while controlling interests command 5x–8x. Multi-specialty ASCs generally achieve slightly higher multiples across the board — minority interests often trade in the 4x–6x range, with controlling interests reaching 6x–8x.

For example, on their earnings call, Surgery Partners has publicly stated they deploy capital at approximately 8x EBITDA multiple for ASC acquisitions. Given that they generally structure their ASC partnerships where they are either a majority owner or have buy-up options to acquire controlling interest in the future – this aligns with the upper end of the ranges above.

The control premium is significant. Buyers acquiring majority ownership gain the ability to direct strategy, operations, and distributions — and they pay accordingly. Minority interest transactions consistently close at lower multiples, reflecting the limited influence that comes with a non-controlling stake.

Two additional factors can meaningfully shift multiples. In states with Certificate of Need (CON) requirements, existing ASCs often command premiums due to regulatory barriers that limit new competition. Conversely, heavy reliance on out-of-network revenue can dramatically reduce value — or eliminate most buyers entirely. Centers with substantial out-of-network exposure often see significant multiple reductions, and many institutional buyers simply won’t pursue them.

The Critical Role of EBITDA in Surgery Center Valuation

EBITDA serves as the cornerstone of surgery center valuation because it provides a clear picture of operational performance independent of capital structure, tax situations, and non-cash accounting items. When investors and buyers evaluate an ASC, they focus on EBITDA as a proxy for cash-generating ability.

Why EBITDA Matters in ASC Valuations

EBITDA eliminates variables that don’t reflect the day-to-day operational success of a surgery center:

Interest Expenses: Removed because the acquiring entity will have its own financing structure. Two identical surgery centers with different debt loads will have the same operational value.

Taxes: Excluded because tax situations vary by entity structure, jurisdiction, and planning strategies. The buyer’s tax position will differ from the seller’s, so pretax earnings provide a cleaner comparison.

Depreciation and Amortization: These non-cash expenses depend on accounting elections (depreciation methodology, useful life assumptions) and whether prior acquisitions created amortizable intangibles. Two operationally identical centers can show very different D&A figures. Removing them allows for apples-to-apples comparison of cash-generating ability.

Controlling Interests vs. Non-Controlling Ownership in EBITDA Analysis

The structure of ownership significantly impacts how EBITDA translates into surgery center valuation:

Controlling Interests hold majority stakes (typically 51% or more) and exercise significant influence over:

- Strategic decision-making

- Operational policies

- Capital allocation

- Management selection

Controlling interests typically command premium valuations because they offer the buyer full operational control and the ability to implement strategic changes.

Non-Controlling Ownership Structures (minority stakes) have limited influence on:

- Day-to-day operations

- Major strategic decisions

- Distribution policies

- Exit timing

Non-controlling interests often face large discounts compared to controlling interests due to lack of control. These discounts, known as discounts for lack of control (DLOC), reflect the diminished value of minority positions.

Selecting the Right EBITDA Measure for Accurate Surgery Center Valuation

Choosing the appropriate EBITDA measure is perhaps the most nuanced aspect of surgery center valuation. Not all EBITDA calculations are created equal, and selecting the wrong measure can significantly misrepresent a center’s true value.

Types of EBITDA in ASC Valuations

Historical EBITDA: Based on actual past performance, typically averaging the previous 12-24 months. This approach is straightforward but may not reflect current conditions or recent operational improvements.

Normalized EBITDA: Adjusts historical EBITDA for one-time events, unusual expenses, or revenues that won’t continue. Common normalizing adjustments include:

- Removing one-time legal settlements or insurance proceeds

- Adjusting for above-market or below-market management compensation

- Eliminating expenses related to ownership changes

- Normalizing supply costs to market rates

Projected EBITDA: Forward-looking estimates based on expected future performance. Used when recent changes (new surgeon partnerships, expanded services, payer contracts, new management fees) haven’t yet fully impacted historical results.

Pro Forma EBITDA: Reflects the EBITDA a center would generate under new ownership or operational assumptions. Critical for platform acquisitions where buyer synergies will materially impact performance.

Key Considerations in EBITDA Selection

The procedural mix within a surgery center significantly influences which EBITDA measure is most appropriate. Centers heavily weighted toward high-margin specialties may show different trajectories than those performing lower-margin procedures.

Ownership structures also dictate EBITDA calculation approaches. Physician-owned centers with physician investors who also serve as surgeons require careful normalization of physician compensation to separate reasonable compensation from distributions of earnings.

Recent acquisitions or partnerships can create complications in EBITDA measurement. If a surgery center recently acquired another facility or added new physician partners, historical EBITDA may not reflect the combined entity’s true earning potential.

Payer contract changes represent another critical factor. New in-network contracts or rate renegotiations that occurred mid-period require projection or pro forma adjustments to accurately represent ongoing earnings capacity.

Selecting the right EBITDA measure is one of the most consequential decisions in any ASC valuation — and one of the most common sources of dispute between buyers and sellers. Nechay Appraisals has extensive experience normalizing and adjusting ASC financials to arrive at a defensible, well-supported value conclusion. Contact us to learn how we approach EBITDA analysis for surgery centers.

Complexities in Determining Surgery Center Valuation Multiples

The process of determining accurate valuation multiples for ASCs involves navigating numerous complexities beyond simple financial formulas. These intricacies stem from the unique characteristics of the healthcare industry and the specific operational dynamics of ambulatory surgery centers.

Regulatory and Compliance Factors

Certificate of Need (CON) States: In states requiring CON approval for new surgery centers, existing ASCs may command premium valuations due to barriers to entry. Limited competition created by CON laws can justify multiples at the higher end of typical ranges.

Stark Law and Anti-Kickback Compliance: Valuation multiples must account for compliance with federal healthcare regulations governing physician ownership and referrals. Centers with ownership structures that create compliance risks may face discounted multiples.

State-Specific Regulations: Some states impose additional requirements on ASC ownership, such as minimum physician ownership percentages or restrictions on corporate practice of medicine. These regulations can impact both marketability and valuation.

Management Agreements and Their Impact

Management service agreements (MSAs) between ASCs and management companies significantly influence surgery center valuation. The terms of these agreements affect both EBITDA calculation and applicable multiples:

Fair Market Value Management Fees: Centers paying market-rate management fees (typically 3-6% of net revenue) generally receive full valuation multiples. The EBITDA reflects sustainable operations under professional management.

Above-Market Management Fees: Some centers have legacy agreements with management fees exceeding market rates. These require EBITDA normalization, adding back the excess fees to reflect true operational performance. However, if the agreement can’t be easily modified, the valuation multiple itself might be reduced to account for the burden.

Integrated Services: Centers where the management company provides significant infrastructure, technology, and operational support may be more dependent on that relationship, potentially affecting multiples if the relationship wouldn’t survive an ownership change.

Procedural Mix and Specialty Concentration

The mix of procedures and specialty concentration within a surgery center creates both opportunities and risks that impact valuation multiples:

Specialty Concentration Risk: Single-specialty centers face greater risk if that specialty experiences reimbursement cuts, regulatory changes, or shifts in care delivery. This concentration risk typically results in slightly lower multiples compared to well-diversified multi-specialty centers.

High-Margin Procedure Mix: Centers performing a high percentage of premium procedures (such as total joints in orthopedics or complex retinal surgeries in ophthalmology) may justify higher multiples due to superior unit economics.

Payor Mix Quality: The distribution between commercial, Medicare, and Medicaid cases significantly impacts both EBITDA and multiples. Centers with 70%+ commercial payor mix typically command premium valuations.

Factors That Influence Surgery Center Valuation

Beyond the basic mathematics of multiples, numerous factors influence the ultimate valuation of ambulatory surgery centers. Understanding these elements helps both buyers and sellers navigate negotiations with realistic expectations.

Revenue Streams and Growth Trends

Consistent revenue growth demonstrates an ASC’s competitive position and market demand. Surgery center valuation improves substantially when centers show:

Year-over-Year Growth: Centers demonstrating 5-10% annual revenue growth typically receive higher multiples than flat or declining facilities. This growth signals strong market position and effective physician recruitment.

Case Volume Trends: Increasing case volumes indicate growing surgeon satisfaction and market share gains. Even if average reimbursement per case remains flat, volume growth drives value.

New Surgeon Recruitment: Recently recruited surgeons who haven’t yet reached full productivity represent future EBITDA growth not reflected in historical numbers. Buyers will pay for this documented pipeline through higher multiples or pro forma EBITDA adjustments.

Operational Efficiency Metrics

Operational excellence directly translates to higher surgery center valuation through both improved EBITDA and multiple expansion:

Operating Margin: High-performing ASCs maintain operating margins of 30-45%. Centers consistently above 35% typically command top-quartile multiples within their size category.

Staff Productivity: Efficient staffing models that optimize patient throughput without compromising quality demonstrate operational sophistication that buyers value. Key metrics include cases per OR per day and revenue per FTE.

Supply Chain Management: Centers with optimized supply costs demonstrate management competence that justifies premium valuations.

Market Position and Competitive Dynamics

The competitive landscape in an ASC’s market significantly influences valuation:

Market Exclusivity: In markets with few competitors or high barriers to entry, existing surgery centers command premium multiples. This is particularly true in CON states or markets where major health systems control most hospital-based outpatient surgery capacity.

Hospital Competition: ASCs facing limited competition from hospital outpatient departments typically enjoy stronger negotiating positions with payors and can maintain pricing power, supporting higher valuations.

Network Adequacy Requirements: In markets where insurance networks have limited ASC capacity, existing in-network centers become essential to payor networks, creating significant strategic value.

Payer Relationships and Contracting

The strength and terms of an ASC’s payer contracts fundamentally drive surgery center valuation:

In-Network vs. Out-of-Network: In-network ASCs with major commercial payors are significantly more marketable and typically command higher valuations. Network access provides volume stability, reduces patient price sensitivity, and lowers collection risk. Out-of-network centers face a narrower buyer pool. Many buyers won’t consider facilities with substantial out-of-network revenue. Those who do often apply meaningful multiple reductions to account for reimbursement uncertainty and regulatory risk.

Contract Terms and Duration: Long-term contracts (3-5 years) with major payors provide revenue visibility that buyers value. Centers with annual contracts or month-to-month arrangements face uncertainty that depresses multiples.

Rate Adequacy: Even with in-network status, the actual contracted rates matter enormously. Centers with rates at or above Medicare demonstrate strong negotiating positions and justify higher valuations.

Facility and Equipment Considerations

Physical assets and their condition impact surgery center valuation through multiple channels:

Facility Ownership vs. Leasing: Centers that own their facilities may include real estate value separate from operational value. However, owned real estate can also create complications if buyers don’t want the real estate included.

Equipment Age and Condition: Modern, well-maintained surgical equipment indicates lower near-term capital requirements. Conversely, aging equipment requiring replacement creates hidden liabilities that reduce effective valuation.

Certificate of Occupancy and Licensing: All necessary licenses, accreditations (AAAHC, AAAASF, or Joint Commission), and permits must be current and transferable. Any compliance gaps can significantly delay or derail transactions.

Expansion Capacity: Physical space for additional operating rooms or procedure rooms represents valuable growth optionality that buyers will pay for, particularly if the center operates near capacity.

Impact of Size on Surgery Center Valuation Multiples

Size represents one of the most significant drivers of valuation multiples in the ASC market. Larger centers consistently command higher multiples than smaller facilities, driven by several economic and strategic factors.

Economies of Scale in ASC Operations

Larger surgery centers achieve operational efficiencies that smaller facilities cannot match:

Fixed Cost Absorption: Administrative overhead, management fees, and compliance costs represent a smaller percentage of revenue as centers scale. A $15 million ASC can spread these fixed costs across more procedures than a $3 million center, resulting in superior margins.

Purchasing Power: Large centers negotiate better pricing on supplies, equipment, and services. These savings directly flow to EBITDA, and the sustainability of these advantages justifies higher multiples.

Staffing Efficiency: Multi-OR centers optimize staffing by sharing pre-op, recovery, and administrative personnel across operating rooms. This flexibility reduces labor costs per case.

Buyer Universe Expansion

Surgery center valuation increases with size partly because larger centers attract more potential buyers:

Institutional Investor Thresholds: Many private equity funds and ASC management companies have minimum EBITDA requirements ($1.5-2 million is common). Centers below these thresholds have limited buyer pools, depressing valuations.

Platform Opportunities: Large centers can serve as platform acquisitions for buyers building regional or national ASC portfolios. Platform assets typically command 0.5-1.0x higher multiples than add-on acquisitions.

Debt Financing Availability: Lenders prefer larger, more stable cash flows. Centers generating $3+ million EBITDA can access more favorable debt financing, allowing buyers to pay higher purchase prices through increased leverage.

State Regulatory Environments

State-level regulations create significant variations in surgery center valuation across different markets:

CON State Premiums: Certificate of Need states like Georgia, North Carolina, and South Carolina restrict new ASC development. Existing centers in these markets command 10-20% higher multiples due to protected market positions.

Ownership Restrictions: States with strict physician ownership requirements or corporate practice of medicine prohibitions limit buyer pools and can depress valuations if buyers must maintain complex ownership structures.

Licensing Flexibilities: Some states allow broad surgical specialties under single licenses while others require specialty-specific approvals. Greater flexibility enhances value by enabling easier service line expansion.

Comprehensive Calculation and Interpretation of ASC Valuation

Accurately calculating surgery center valuation requires systematic analysis of historical performance, market positioning, and future potential. While the basic formula (EBITDA × Multiple) appears simple, proper execution demands rigorous financial analysis.

Step-by-Step Valuation Calculation

Step 1: Determine Base EBITDA

Start with historical EBITDA, typically averaging the most recent 12-24 months. For centers with seasonal variations or recent changes, weighted averages favoring recent periods may be appropriate.

Step 2: Normalize EBITDA

Apply normalization adjustments for:

- Non-recurring expenses (legal settlements, equipment write-offs)

- Owner/physician compensation above or below market rates

- Related-party transactions at non-market terms

- Excess or deferred maintenance expenses

Step 3: Apply Pro Forma Adjustments

Incorporate documented changes not yet reflected in historical results:

- New payer contracts with known rate changes

- Recently recruited physicians with projected case volumes

- Operational improvements already implemented but not yet flowing through financials

- Eliminated services or procedures no longer performed

Step 4: Select Appropriate Multiple

Choose the multiple based on:

- Center size and EBITDA level

- Specialty mix and concentration

- Market position and competitive dynamics

- Payer mix and contract quality

- Recent comparable transactions

- Control level (majority vs. minority interest)

Step 5: Calculate Enterprise Value

Enterprise Value = Normalized/Pro Forma EBITDA × Selected Multiple

Step 6: Adjust for Assets and Liabilities

Add: Excess cash, marketable securities Subtract: Interest-bearing debt, unfunded liabilities Consider: Working capital requirements

Interpreting Valuation Results

The calculated surgery center valuation represents a starting point for negotiations rather than a definitive price. Several interpretive factors matter:

Valuation Ranges: Professional valuations typically present ranges (e.g., $12-14 million) rather than point estimates, reflecting uncertainty in assumptions and multiple selection.

Control Premiums: Minority interests typically require discounts for lack of control compared to controlling interests, reflecting the limited influence over operations and strategic decisions.

Marketability Discounts: Minority interests in closely-held ASCs face significant marketability challenges, often warranting 25-40% discounts from a pro-rata share of value.

Transaction-Specific Factors: Strategic buyers may pay premiums for unique synergies, network gaps filled, or competitive positioning achieved through the acquisition.

Comparing Different Surgery Center Valuation Approaches

While EBITDA multiples common ASC valuations, other methodologies provide important perspectives and validation points. Understanding these alternatives enhances confidence in valuation conclusions.

Transaction Multiples Approach

The transaction multiples methodology examines recent sales of comparable surgery centers to derive market-based multiples:

Strengths:

- Reflects actual prices paid by willing buyers and sellers

- Incorporates current market sentiment and capital availability

- Most directly comparable to the subject center

Limitations:

- Limited publicly available ASC transaction data

- Difficulty finding truly comparable transactions

- Transaction-specific factors (buyer synergies, competitive dynamics) may not apply

Application: Most useful for centers with clear comparables in specialty, size, and market characteristics. Requires access to proprietary transaction databases or industry relationships to obtain meaningful data

Alternative Transaction Multiples: While EBITDA multiples dominate ASC transactions, other metrics appear in certain contexts:

Disclaimer: The valuation multiples presented here are for educational purposes only and do not constitute valuation advice or represent the professional opinion of Nechay Appraisals or its analysts. For advice specific to your practice, consult a qualified valuation professional.

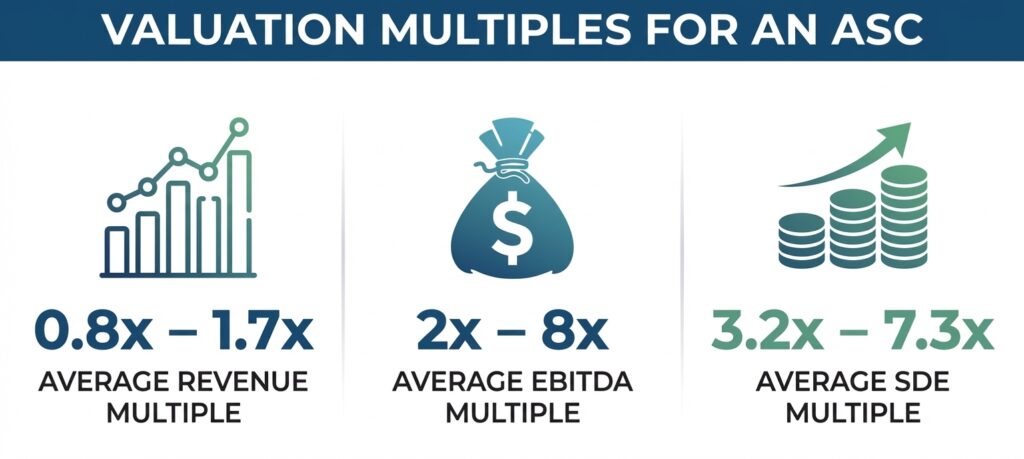

- Revenue Multiples: Sometimes used. Typical range: 0.8x–1.7x revenue.

- SDE (Seller’s Discretionary Earnings) Multiples: Occasionally applied to smaller, owner-operated centers. Typical range: 3.2x–7.3x SDE.

These alternatives are less common but can be useful reference points when EBITDA-based analysis is problematic.

Cost Approach Valuation

The cost approach estimates surgery center valuation based on the replacement cost of physical assets and the investment required to replicate the operating center:

Methodology:

- Calculate cost to replicate leasehold improvements

- Add replacement cost of medical and office equipment

- Include working capital requirements

- Add regulatory approval costs (e.g., CON applications, licensing, accreditation)

- Add value of identifiable intangible assets (assembled workforce, payer contracts, favorable leases)

- Apply depreciation for physical, functional, and economic obsolescence

- Subtract liabilities, adjusted to fair market value where necessary

Strengths:

- Provides floor value for established centers

- Useful when subject center is underperforming and buyer might rebuild

- Important in marital dissolutions or tax disputes, where courts may require asset-based support or need to distinguish between personal and enterprise goodwill

Limitations:

- Doesn’t reflect earning power or market position

- Typically produces values below market multiples for profitable centers

- Difficult to quantify intangible assets (payer contracts, physician relationships, reputation)

Application: The cost approach rarely drives ASC valuations in typical transactions but serves as a sanity check. If market-based multiples produce values below replacement cost for a profitable center, the valuation methodology likely needs reconsideration – or the center is underperforming.

Discounted Cash Flow (DCF) Model

The DCF approach values a surgery center based on projected future cash flows discounted to present value:

Methodology:

- Project 5-10 years of detailed cash flows including:

- Revenue forecasts by specialty/procedure

- Detailed expense projections

- Capital expenditure requirements

- Working capital changes

- Calculate terminal value at projection end

- Discount all cash flows and terminal value to present using weighted average cost of capital (WACC)

Strengths:

- Most theoretically sound valuation method

- Captures center-specific growth trajectories

- Explicitly accounts for risk through discount rate

- Flexible enough to model complex scenarios

Limitations:

- Highly sensitive to assumptions (growth rates, margins, terminal multiples, discount rates)

- Requires detailed forecasting often unavailable for smaller centers

- More time-intensive than multiples approaches

- Can appear overly precise given inherent uncertainties

Application: DCF is most valuable for large, complex surgery centers with documented growth initiatives, new service lines, or significant capital investment programs. It’s particularly useful when historical performance poorly predicts future results due to major changes underway.

Reconciling Multiple Valuation Approaches

Best practice in surgery center valuation involves applying multiple methodologies and reconciling the results:

Triangulation: When market multiples, DCF, and (where relevant) cost approach all produce values within 15-20% of each other, confidence in the valuation conclusion strengthens.

Weighted Analysis: More weight should be given to approaches most relevant to the transaction context. For typical going-concern sales, market multiples and/or income approach deserve primary weight. For litigation or tax purposes, cost approach may receive more consideration.

Sensitivity Testing: Varying key assumptions (multiples, growth rates, discount rates) within reasonable ranges demonstrates the valuation’s robustness and identifies the drivers most critical to value.

Industry Standards and Benchmarks for Surgery Center Valuation Multiples

Understanding industry benchmarks helps contextualize individual surgery center valuations and supports negotiations with data-backed expectations.

National ASC Market Trends

The ASC industry has experienced significant consolidation over the past decade, influencing valuation multiples:

Private Equity Investment: Increased institutional capital seeking ASC investments has driven multiple expansion, particularly for high-quality, platform-scale centers. Well-positioned ASCs now routinely command multiples that would have been considered exceptional 5-10 years ago.

Health System Strategies: Hospital systems increasingly view ASCs as strategic assets for value-based care initiatives and market positioning. Health system buyers sometimes pay strategic premiums above private market multiples.

Management Company Platforms: Major ASC management companies continue aggressive acquisition strategies, providing consistent buyer demand that supports strong valuations, particularly for centers that fit their specialty focus and geographic preferences.

Benchmarking by Ownership Structure

Different ownership models show distinct valuation patterns:

Physician-Owned Centers: Traditional physician-owned ASCs with 51%+ physician ownership typically trade at mid-range multiples unless exceptional performance or market position justifies premiums.

Joint Venture with Health Systems: Hospital joint ventures often show lower profitability due to hospital infrastructure costs but may receive premium multiples from strategic buyers seeking health system relationships.

Management Company Majority Ownership: Centers where management companies hold controlling stakes sometimes trade at lower multiples to physician-controlled centers due to physician retention risk and reduced physician alignment incentives.

Key Considerations When Valuing Surgery Centers

In transaction contexts valuation analysis extends beyond financial calculations into operational and legal due diligence. While a formal appraisal focuses on determining fair market value, buyers and sellers must also evaluate factors that could affect deal execution or post-closing performance.

Due Diligence Priorities

Thorough due diligence uncovers issues that impact both EBITDA calculations and appropriate multiples:

Financial Audit: Verify historical financial statements, EBITDA calculations, and the sustainability of reported performance. Look for:

- Revenue recognition policies and any aggressive accounting

- Expense classifications and potential misallocations

- Related-party transactions that may not survive ownership change

- Working capital requirements and seasonal patterns

Physician Stability: ASC value derives primarily from physician utilization. Critical due diligence includes:

- Physician age demographics and succession planning

- Case volume concentration (what percentage comes from top 3 physicians?)

- Physician satisfaction and retention history

- Non-compete agreements and enforceability

- Exclusive use provisions or commitments

Payer Contract Review: Detailed analysis of all payer contracts including:

- Contract terms, rates, and renewal dates

- Change of control provisions that might trigger renegotiation

- Rate escalators or de-escalators

- Volume commitments or penalties

- Out-of-network versus in-network status

Regulatory Compliance: Comprehensive compliance review covering:

- Medicare certification and any survey deficiencies

- State licensure and accreditation status

- Stark Law and Anti-Kickback Statute compliance

- HIPAA and data security measures

- Employment and HR compliance

Deal Structure Considerations

How a transaction is structured significantly impacts effective surgery center valuation:

Asset vs. Stock Purchase: Asset purchases allow buyers to step up depreciation basis and avoid inheriting unknown liabilities but may trigger tax inefficiencies for sellers. Stock purchases are often cleaner but carry more risk for buyers.

Earnouts and Contingent Consideration: When there’s disagreement between buyer and seller on future performance, earnouts based on achieving EBITDA or revenue targets can bridge valuation gaps.

Physician Rollover Equity: Many ASC transactions involve physicians rolling over a portion of their equity into the new ownership structure. This alignment mechanism reassures buyers about physician commitment and helps physicians participate in future value creation.

Employment and Service Agreements: Medical director agreements, physician employment contracts, and non-compete provisions all affect valuation by ensuring physician continuity and protecting against competition.

Minority Interest Valuation Challenges

Valuing minority interests in surgery centers presents unique challenges:

Lack of Control Discounts: Minority shareholders cannot control operations, elect boards, or force liquidity events. When valuing a minority interest by first determining control-level value and then adjusting downward, a discount for lack of control (DLOC) may be applied. However, if the appraiser uses a direct minority valuation methodology — valuing the actual cash flows a minority holder receives — little or no DLOC may be necessary since the lack of control is already reflected in the projected distributions.

Lack of Marketability Discounts: Unlike publicly traded securities, minority ASC interests cannot be quickly sold. This illiquidity can warrant DLOM of 25-40% from an otherwise marketable interest.

Cumulative Discounts: When both DLOC and DLOM apply, the combined discount can reach 45-60%, meaning a 20% minority interest in a $10 million ASC might be worth only $800,000-$1,100,000 rather than the $2,000,000 pro-rata calculation.

Buy-Sell Agreement Terms: Existing shareholder agreements may dictate valuation methods, creating price ceilings or floors that override market-based valuations.

The Value of Consulting with Surgery Center Valuation Experts

Given the complexity and financial stakes involved, engaging experienced valuation professionals provides significant benefits for both buyers and sellers.

When Professional Valuations Are Essential

Professional surgery center valuation reports become critical in several scenarios:

Transaction Planning: Before marketing a center or beginning acquisition discussions, an independent valuation establishes realistic expectations and strengthens negotiating positions.

Tax and Estate Planning: IRS regulations require qualified appraisals for estate tax purposes, charitable contributions, and certain ownership restructurings. Only certified appraisers can provide opinions that satisfy IRS requirements.

Shareholder Disputes: When shareholders disagree on buyout terms or fair value, an independent valuation can facilitate resolution or provide evidence in litigation.

Financial Reporting: Some physician-owned ASCs require periodic valuations for financial statement purposes, particularly when there are complex ownership structures or fair value measurements required.

SBA Lending: Small Business Administration loans often require independent valuations as part of the underwriting process.

Qualifications to Seek in Valuation Experts

Not all business appraisers have the specialized knowledge required for surgery center valuation:

Healthcare Industry Experience: Look for appraisers with extensive ASC-specific experience who understand the operational nuances, regulatory environment, and market dynamics unique to ambulatory surgery.

Professional Credentials: Relevant certifications include:

- ASA (Accredited Senior Appraiser)

- ABV (Accredited in Business Valuation)

- CVA (Certified Valuation Analyst)

- CFA (Chartered Financial Analyst)

Transaction Database Access: Expert valuators maintain access to proprietary databases of ASC transactions, providing the market intelligence necessary for credible multiples analysis.

Regulatory Knowledge: Deep understanding of healthcare regulations (Stark, Anti-Kickback, CON laws, CMS requirements) ensures valuations reflect compliance considerations.

Working Effectively with Valuation Professionals

Maximize the value of professional engagements by:

Providing Complete Information: Supply comprehensive financial statements, payer contracts, physician agreements, and operational data. Incomplete information forces appraisers to make assumptions that may not align with reality.

Articulating Purpose: Different valuation purposes (transaction, tax, litigation) require different approaches and reporting standards. Be explicit about how the valuation will be used.

Asking Questions: Understand the methodology, assumptions, and sensitivities in the valuation. A good appraiser welcomes questions and explains their reasoning.

Considering Ranges: Valuation isn’t an exact science. Credible appraisers present ranges and discuss the factors that might push value toward the high or low end.

Conclusion: Mastering Surgery Center Valuation for Successful Transactions

Surgery center valuation combines art and science, requiring both rigorous financial analysis and nuanced judgment about market conditions, operational quality, and strategic positioning. While EBITDA multiples provide the primary framework, successful valuations account for the dozens of factors that influence both sustainable earnings and appropriate multiples.

Whether you’re a physician-owner contemplating selling your equity, an investor evaluating acquisition opportunities, or a healthcare system considering ASC partnerships, understanding these valuation principles empowers better decision-making and more successful transactions.

The key takeaways for surgery center valuation include:

- Multiples vary significantly based on size, specialty, market, and operational performance, typically ranging from 2x to 8x EBITDA

- EBITDA selection matters enormously – historical, normalized, and pro forma EBITDA can vary by 20-30% or more

- Due diligence is critical – physician stability, payer contracts, and regulatory compliance can make or break value

- Size drives multiples – larger centers command premium valuations through economies of scale and broader buyer appeal

- Professional expertise pays – qualified valuation experts provide credibility, market intelligence, and technical expertise that justify their fees many times over

As the ASC industry continues consolidating and evolving, staying informed about valuation trends and best practices becomes increasingly important. The centers that achieve premium valuations share common characteristics: strong operational performance, diversified revenue streams, stable physician relationships, and advantageous market positioning.

For specific guidance on your surgery center valuation needs, contact Nechay Appraisals. We specialize in ASC and medical practice valuations, and work hard to deliver appraisals that are thorough, well-supported, and useful — whether you’re planning a transaction, resolving a dispute, or simply trying to understand what your interest is worth. Schedule a free consultation today.

Frequently Asked Questions About Surgery Center Valuation

What Are Surgery Center Valuation Multiples?

Surgery center valuation multiples are financial ratios used to determine the market value of ambulatory surgery centers by comparing specific financial metrics (most commonly EBITDA) to the center’s enterprise value. These multiples provide a standardized method for evaluating ASCs against comparable facilities and recent transaction data in the healthcare market.

How Are Surgery Center Valuation Multiples Calculated?

Valuation multiples are calculated by dividing the surgery center’s value — expressed as either Market Value of Invested Capital (MVIC) or Enterprise Value (EV) — by a specific financial metric. MVIC includes equity value plus interest-bearing debt and treats cash as an operating asset. Enterprise Value is similar but excludes cash. The most common calculation is:

Valuation Multiple = MVIC (or EV) ÷ EBITDA

For example, if a surgery center sells for $20 million (MVIC) and generates $3 million in EBITDA, the transaction multiple is 6.67x EBITDA.

Why Are Surgery Center Valuation Multiples Important?

Valuation multiples are important because they provide a quick, standardized method to estimate ASC value and compare it to similar facilities in the market. Multiples allow buyers and sellers to establish reasonable price expectations based on actual market transactions rather than theoretical calculations. They also facilitate comparison across different sizes and specialties of surgery centers.

What Factors Influence Surgery Center Valuation Multiples?

Multiple factors influence ASC valuation multiples including:

● Size and scale: Larger centers command higher multiples vs. smaller facilities

● Specialty mix: Multi-specialty centers typically receive premium multiples compared to single-specialty

● Payer relationships: In-network status and contract quality significantly impact value

● Location: CON states and markets with limited competition support higher multiples

● Financial performance: Operating margins, growth trends, and profitability drive multiples

● Physician stability: Surgeon age, retention, and case volume concentration affect value

How Do Surgery Center Valuation Multiples Compare to Other Valuation Methods?

Unlike discounted cash flow analysis which projects future cash flows, or cost approach which estimates replacement value, surgery center valuation multiples focus on comparing the ASC to similar entities based on current market conditions. Multiples like MVIC/EBITDA or Price-to-Revenue ratios offer straightforward, market-based assessments that are particularly practical for typical ASC transactions. However, for complex situations involving major growth initiatives or unique circumstances, DCF analysis provides more nuanced insights.

What Is the Difference Between In-Network and Out-of-Network ASC Valuations?

In-network surgery centers with contracts with major commercial insurance payors receive higher valuations than comparable out-of-network facilities. In-network status provides:

● More predictable patient volume

● Reduced patient price sensitivity

● Lower bad debt and collection costs

● Easier physician recruitment

● Greater strategic value to buyers

Out-of-network centers may achieve higher per-case reimbursement but face volume uncertainty and greater regulatory scrutiny that typically results in lower overall valuations.

Are There Different Types of Surgery Center Valuation Multiples?

Yes, several types of multiples are used in ASC valuations:

● MVIC/EBITDA: Most common, typically 2x-8x depending on factors

● MVIC/Revenue: Less common, useful when EBITDA is distorted

● MVIC/SDE (Seller’s Discretionary Earnings): Sometimes used for small, physician-owned centers

● Price/Earnings: Occasionally used but less relevant for ASCs due to varying tax structures and capital expenses

EBITDA multiples dominate the market because they best reflect operational performance independent of financing, tax, and accounting decisions.

How Do Single-Specialty and Multi-Specialty Centers Compare in Valuation?

Multi-specialty surgery centers generally command higher valuation multiples than single-specialty centers. For controlling interests, multi-specialty facilities typically trade in the 6x–8x EBITDA range, while single-specialty centers fall in the 5x–8x range. For minority interests, multi-specialty centers often see 4x–6x, and single-specialty centers 3x–5x. The premium for multi-specialty reflects:

● Diversification reduces specialty-specific risks

● Multiple physician specialties provide revenue stability

● Broader procedural capabilities attract more strategic buyers

● Better positioned for value-based care arrangements

● Less vulnerable to specialty-specific reimbursement changes

However, well-positioned single-specialty centers in high-margin specialties (like ophthalmology) can achieve premium valuations comparable to multi-specialty facilities.

What Role Does Size Play in Surgery Center Valuation?

Size is one of the most significant drivers of valuation multiples. Larger surgery centers consistently command higher multiples because:

● Economies of scale improve operating margins

● Broader buyer universe including institutional investors

● Better financing availability allows buyers to pay higher prices

● Platform acquisition value for buyers building portfolios

● Reduced business risk from larger, more diverse patient volumes

When Should You Hire a Surgery Center Valuation Expert?

Professional valuation experts should be engaged for:

● Transaction planning: Before marketing or beginning acquisition discussions

● Tax compliance: Estate planning, charitable contributions, or IRS-required appraisals

● Shareholder disputes: Resolving disagreements on fair value for buyouts

● Financial reporting: Periodic valuations for complex ownership structures

● SBA financing: Independent valuations often required for loan approval

● Strategic planning: Understanding value drivers to maximize future sale price

The cost of professional valuation (typically $4,000-$10,000) is minimal compared to the financial stakes in most ASC transactions. For specific guidance on your surgery center valuation needs, contact Nechay Appraisals. We specialize in ASC and medical practice valuations, and work hard to deliver appraisals that are thorough, well-supported, and useful — whether you’re planning a transaction, resolving a dispute, or simply trying to understand what your interest is worth. Schedule a free consultation today.